Taxing the Symptom, Ignoring the Cause.

Why Changing CGT Won’t Fix Australia’s Housing Crisis

The Policy Shift That Misses the Point

The Federal Government’s renewed focus on adjusting Capital Gains Tax (CGT) concessions for investment properties, while leaving other asset classes largely untouched, has reignited a familiar narrative:

Reduce investor participation, and first home buyers will finally get their chance.

At face value, it’s politically attractive.

But as with many housing interventions, it risks targeting the symptom rather than the structural cause.

Because the uncomfortable, and very obvious, truth is this:

Australia does not have an investor problem. It has a supply problem.

Supply: The Core Issue We Keep Avoiding

Across Australia, particularly in high-demand markets like Melbourne and Sydney, housing supply has consistently lagged population growth.

Key pressures include:

Population growth and migration rebounding strongly post-COVID

Construction capacity constraints (labour shortages, material costs)

Planning and zoning bottlenecks

Lengthy development approval (DA) processes

Even conservative estimates show Australia needs hundreds of thousands of additional dwellings over the next decade just to stabilise affordability.

In addition to this, Australia has recorded its third-highest February intake of overseas arrivals, with almost 100,000 people moving to the country. New figures from the Australian Bureau of Statistics show 96,110 net permanent and long‑term (NPLT) arrivals landed in February 2026, amounting to about 3432 people a day.

Yet policy attention continues to skew toward demand-side interventions - tax settings, grants, and incentives - rather than unlocking supply at scale.

The Myth: “Fewer Investors = More First Home Buyers”

The idea that reducing investors will automatically create opportunities for first home buyers is overly simplistic.

In reality:

Investors and owner-occupiers do not operate in identical segments of the market

Many investor-owned properties are rental stock, not vacant inventory

Removing investors does not create new dwellings

Instead, what happens is a reallocation, not expansion, of supply.

At the same time, broader macro conditions complicate the equation:

Higher interest rates have already reduced borrowing capacity for both investors and first home buyers

Strong immigration levels continue to drive demand for both ownership and rental markets

Construction pipelines remain constrained, limiting new stock

So, while investor demand may soften, first home buyers are not necessarily better positioned to step in.

Development Approvals: The Hidden Bottleneck

If supply is the issue, then the development pipeline is where attention should be focused.

Across Australia, development approval timelines are widely recognised as a major constraint:

In Victoria, planning approvals for medium-density projects can often take 12–24 months or longer

Comparable delays exist in NSW and Queensland, particularly in urban infill zones

Appeals, overlays, and local objections frequently extend timelines furtherThere is also growing concern about:

Backlogs of unapproved or stalled DAs

Projects approved but not financially viable under current cost conditions

Developers delaying commencement due to uncertainty and risk

The result?

| Supply is not just slow, it is structurally constrained.

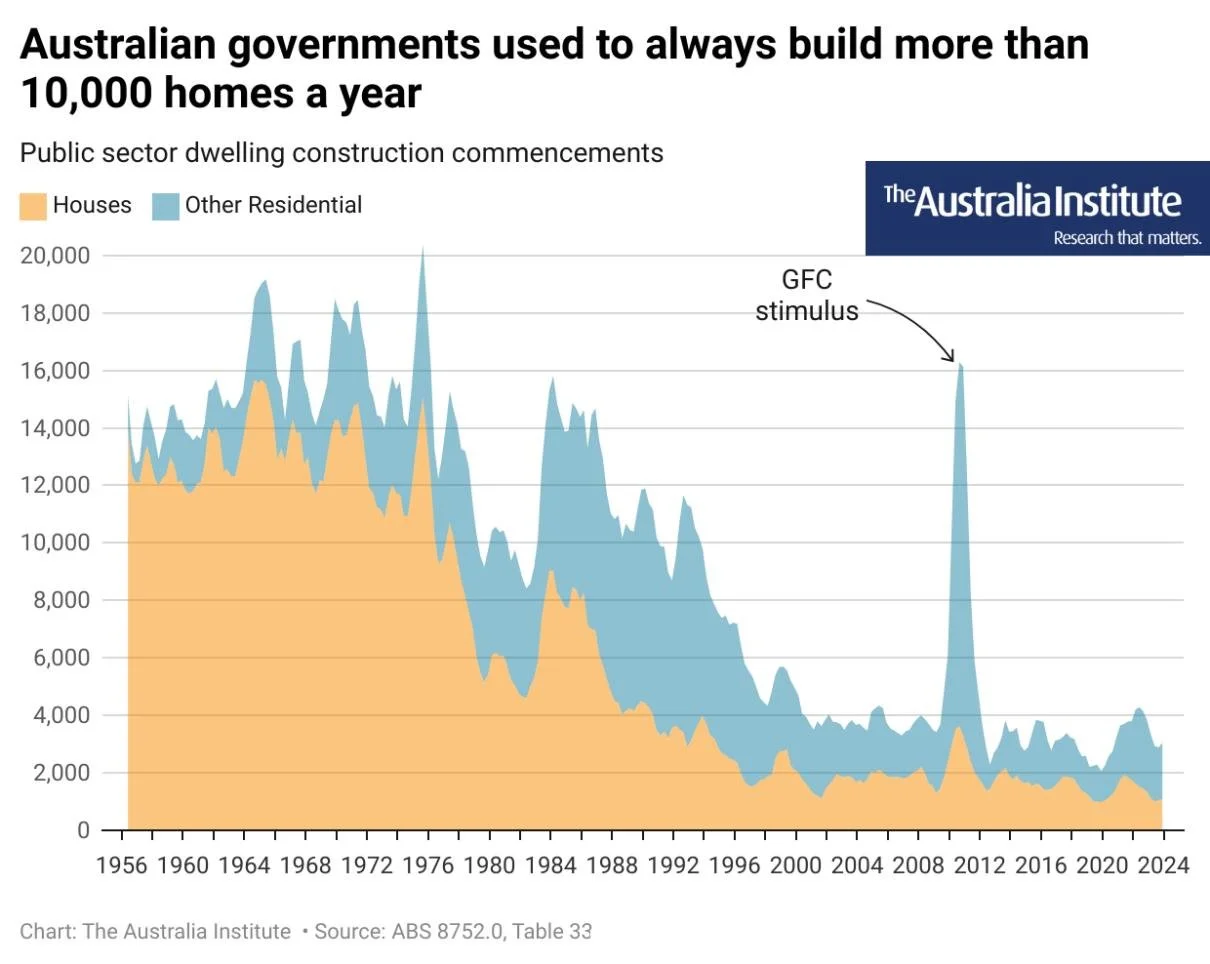

Public Housing: A Critical but Underpowered Lever

Public and social housing should play a stabilising role in the system.

However:

Australia’s public housing stock sits at historically low levels relative to population

Waiting lists remain long and growing

Delivery pipelines are slow and fragmented across jurisdictions

Even where governments commit funding, delivery timelines often stretch years, meaning relief is delayed.

If investor participation is reduced before public housing supply ramps up, the pressure on the rental market intensifies.

The Rental Market Impact: A Predictable Outcome

Reducing investor incentives has a direct and immediate effect:

Less investor participation = less rental supply

And the consequences are already visible in many markets:

Rising rents

Lower vacancy rates

Increased competition among tenants

Greater pressure on vulnerable households

This is not theoretical - it is observable.

A policy designed to help first home buyers can unintentionally:

Worsen rental affordability

Displace lower-income households

Increase demand for already constrained public housing

If Not Property, Where Does the Capital Go?

Investment capital does not disappear, it reallocates.

If residential property becomes less attractive due to tax changes, capital is likely to shift toward:

Equities (domestic and international)

Commercial property

Alternative assets (private equity, infrastructure)

Offshore investments

This raises broader economic questions:

Does this reduce domestic housing investment at a critical time?

Does it redirect capital away from essential infrastructure (housing)?

Could it contribute to asset price inflation elsewhere?

In effect, the policy may not reduce speculation, it may simply move it.

There is also a structural inconsistency in how CGT changes risk reshaping investor behaviour.

By reducing concessions or increasing the tax burden on long-held residential property, while leaving other asset classes comparatively untouched, policy may inadvertently favour shorter-term, transactional investment over long-term stewardship.

An investor who enters the market, renovates, and exits within a relatively short timeframe can still realise gains through turnover and value-add strategies, often recycling capital quickly.

By contrast, a long-term investor who holds property for 10 years or more, providing stable rental supply over that period, faces a cumulative exposure to tax changes, holding costs, and policy uncertainty that erodes overall returns.

The net effect is perverse:

the system risks incentivising churn over stability, rewarding those who treat housing as a short-term trade rather than those who contribute to sustained rental supply.

A Better Path Forward: Structural, Not Symbolic Reform

If the objective is genuine affordability and availability, the policy response needs to shift from optics to outcomes.

1. Accelerate Development Approvals

State governments should enforce statutory timeframes for DA decisions

Streamline planning overlays and reduce duplication

Introduce “fast-track” pathways for high-priority housing projects

2. Align Immigration with Construction Capacity

Maintain migration, but prioritise skilled trades critical to housing delivery

Ensure workforce supply matches housing demand creation

3. Expand Public & Social Housing At Scale

Move beyond incremental programs

Partner with institutional capital for build-to-rent and social housing models

Set measurable delivery targets tied to population growth

4. Avoid Demand-Side Inflation

Grants and incentives often push prices higher without increasing supply

Focus instead on reducing delivery costs and barriers

5. Maintain a Balanced Investor Ecosystem

Investors are not the enemy. They are a core part of the housing system

Policy should aim for stability and predictability, not volatility

The Bottom Line

Changing CGT settings for property, while politically appealing, does little to address the fundamental imbalance in Australia’s housing system.

In the same way as Winston Churchill said, “For a nation to try to tax itself into prosperity is like a man standing in a bucket and trying to lift himself up by the handle”, you cannot tax your way out of a supply shortage.

Until policy squarely addresses:

Planning constraints

Construction capacity

Public housing delivery

Population alignment

…housing affordability will remain out of reach for many Australians.

And in the meantime, well-intentioned reforms risk making the system more fragile, not fairer.