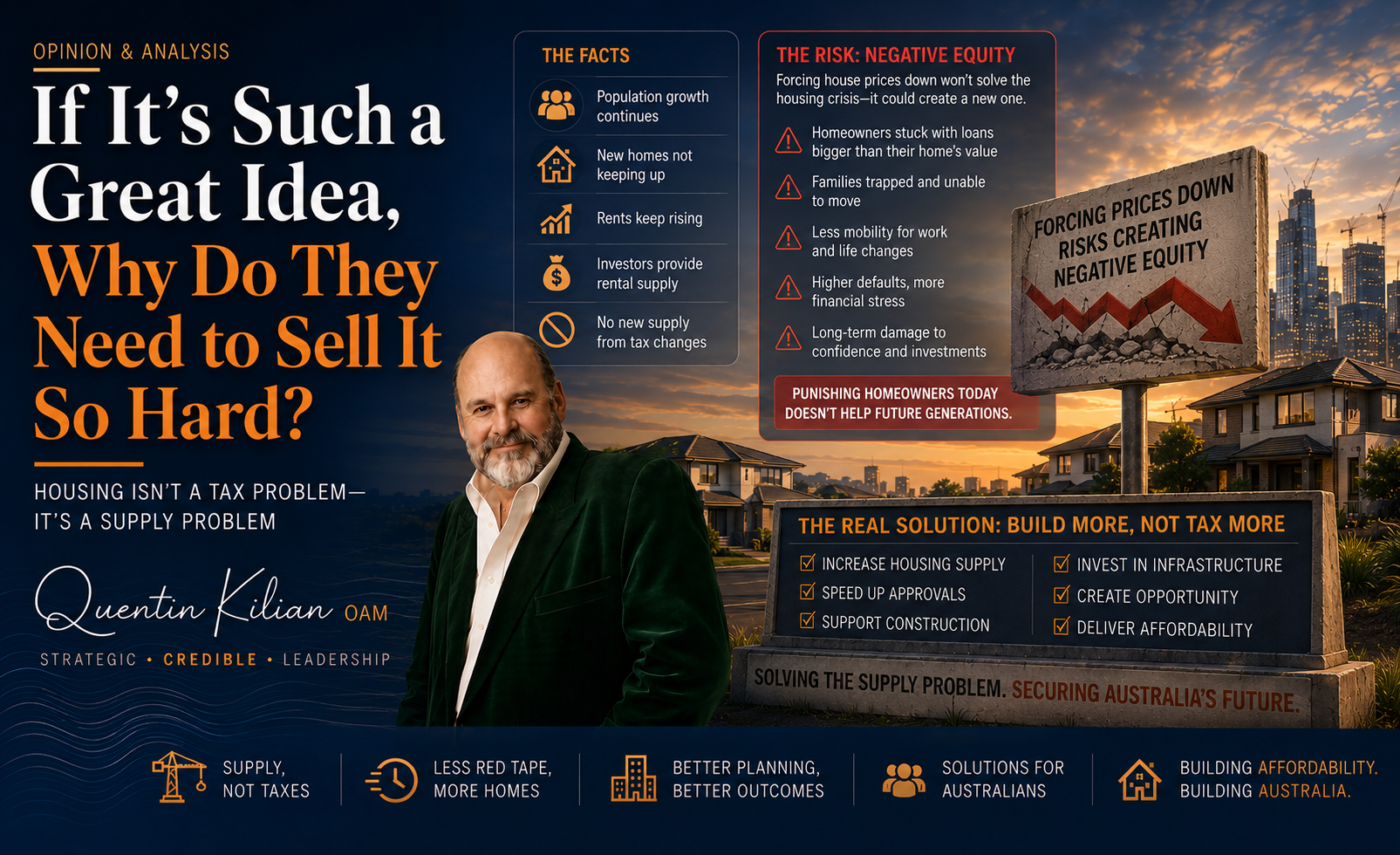

If It's Such a Great Idea, Why Do They Need to Sell It So Hard?

There is an old saying in business: if someone has to work too hard to convince you, perhaps the product is not as good as they claim.

Whether it is a used car salesman, an investment spruiker, or a real estate agent pushing a property that has been sitting on the market too long, our instincts tell us to be cautious when the sales pitch becomes relentless.

That is why I am increasingly concerned about the Federal Government's proposed changes to Capital Gains Tax and Negative Gearing. (That’s not to say I am not concerned about these items, I am, but that is an argument for another time.)

Not necessarily because of the detail. Because of the intensity of the sales campaign.

The Prime Minister and Treasurer seem determined to tell Australians - almost daily - that these changes are unquestionably good for housing affordability, good for first-home buyers, and good for the nation.

Whenever politicians spend more time selling a policy than explaining its risks, Australians should pay attention.

Because every major economic reform produces winners and losers.

The question is not whether there will be consequences.

The question is whether the Government is being honest about them.

The Promise

The Government's argument seems simple – ‘Reduce the tax advantages available to residential property investors and more homes will become available to owner-occupiers.’

In theory, fewer investors means less competition for first-home buyers.

It sounds logical. Right?

But housing markets are rarely that simple.

For every property sold by an investor, another person must buy it.

The ownership changes. The dwelling itself does not.

But in reality, that assumes the theory will work in practice and that solving the problem is really that simplistic. But it is not. Australia's housing shortage is fundamentally a supply problem, not an issue of who owns that property.

Changing who owns existing housing stock does little to increase the number of homes available.

The Reality

The Government insists investors are the problem.

Yet investors currently provide the overwhelming majority of Australia's private rental housing.

When investors leave the market, rental stock falls. When rental stock falls, rents rise.

This is not ideology. It is basic economics.

If enough investors decide that residential property is no longer attractive, we will likely see:

Fewer rental properties available.

Higher rents for tenants.

Reduced investment in maintenance and upgrades.

Less private capital entering housing markets.

Increased pressure on governments to provide social housing.

The Government may achieve lower house prices, and in fact we are already seeing prices falling across Australia, but lower house prices are not the same thing as improved affordability.

A home that is 5 per cent cheaper is still unaffordable if finance remains difficult to obtain, deposits remain substantial, and supply remains constrained.

The Negative Equity Trap

Perhaps the greatest risk in this entire debate is one that receives remarkably little attention: negative equity.

The Government appears comfortable talking about lower house prices as though they are inherently beneficial.

But what happens if prices fall significantly?

For many Australians, particularly those who purchased recently, a substantial decline in property values could leave them owing more on their mortgage than their home is worth.

That is negative equity.

Consider a young couple purchasing their first home for $800,000 under the Federal Government's Home Guarantee Scheme.

They contribute a 5 per cent deposit of $40,000 and borrow the remaining $760,000. Because the Government guarantees part of the loan, they are not required to pay Lenders Mortgage Insurance.

At settlement, they effectively own just 5 per cent of the property.

Now imagine housing values fall by 10 per cent following policy changes designed to suppress prices.

Their home is now worth approximately $720,000.

Their mortgage, however, remains close to $760,000.

Almost overnight, they have moved from being homeowners to being in negative equity.

They owe around $40,000 more than the property is worth.

If they need to relocate for work, divorce, illness or family reasons, they may be unable to sell without finding tens of thousands of dollars to clear the remaining debt.

They cannot easily refinance.

They may struggle to access additional finance

A larger correction could leave them effectively trapped.

They cannot sell without crystallising a loss.

And they are precisely the Australians the Government says it is trying to help.

It’s The Economy, Stupid

The Australian economy is heavily exposed to residential property. Banks, superannuation funds, retirees, small business owners and everyday homeowners all have significant interests tied to housing values.

A moderate market correction may be manageable.

A policy-induced decline that creates widespread negative equity could have consequences extending far beyond the property market.

Consumer confidence falls.

Household spending contracts.

Business investment weakens.

Banks tighten lending standards.

Economic growth slows.

History shows that housing downturns can become broader economic problems remarkably quickly.

Australia witnessed the consequences of housing market weakness during the early 1990s recession, while overseas examples such as the United States, Ireland and parts of Europe during the Global Financial Crisis demonstrate how quickly housing corrections can become broader economic problems.

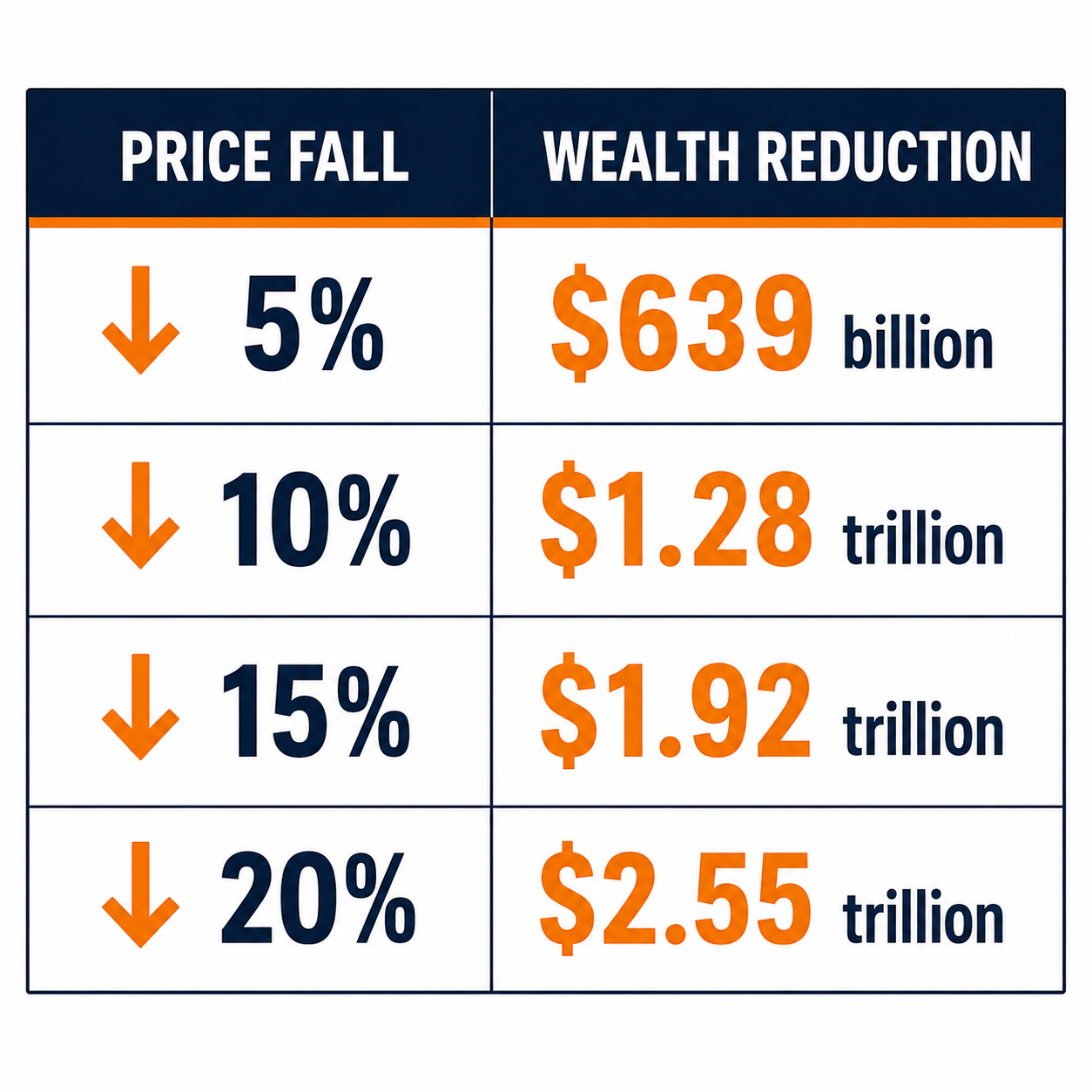

The latest official figures show that the Australian residential housing market is worth approximately $12.8 trillion, with the ABS reporting a total dwelling value of $12.77 trillion in the March Quarter 2026.

To put that in context:

Australian GDP is approximately $3 trillion per annum.

Residential housing is worth more than four times annual GDP.

Around 56% of Australian household wealth is tied up in residential property.

Outstanding residential mortgages are approximately $2.6 trillion, meaning most of the housing stock is owned with substantial equity.

And yet the Government insists their proposed reforms will make housing more affordable. Perhaps they will for some buyers.

But if the pathway to affordability involves pushing existing Australians into negative equity, then the question becomes far more complex.

Forcing Housing Prices Down

If government policy deliberately causes a significant reduction in housing values, the impact extends far beyond investors.

Assuming the housing market is worth $12.8 trillion, what would a fall in housing values doe to the overall economy?

A 10% fall would effectively remove approximately $1.3 trillion of household wealth from Australian balance sheets.

The Tax Question Nobody Wants to Discuss

There is another issue that receives far less attention.

Australians are already heavily taxed.

The Australian Bureau of Statistics reports that average full-time earnings are now approximately $2,051 per week, or around $106,600 annually.

On that income, an average worker might pay:

Income tax.

Medicare Levy.

GST on everyday spending.

Fuel excise.

Vehicle registration charges.

Council rates through housing costs.

Insurance taxes and duties.

Alcohol and tobacco excise (where applicable).

Stamp duty on property purchases.

Land tax indirectly through rents.

Payroll tax indirectly through business costs.

The result is that many Australians surrender well over one-third of their economic output to government (more if they are a high income earner) before they have paid a mortgage, bought groceries, or saved for retirement.

Yet the answer from Canberra is almost always the same:

More tax changes.

More intervention.

More market manipulation.

Rarely do we hear discussion about truly reducing the tax burden that already constrains households and businesses.

The Forgotten First-Home Buyer

Ironically, first-home buyers may discover they are not the primary beneficiaries of these reforms.

If investors are pushed towards newly constructed housing, they will be competing directly with aspiring homeowners for the same new developments.

At the same time, Australia's population continues to grow strongly, driven largely by migration.

Demand for housing does not disappear because investors retreat.

It simply shifts.

The young family trying to buy their first home may find themselves competing against other owner-occupiers, migrants, and investors concentrated into a smaller segment of the market.

That is not necessarily a recipe for affordability.

But Trust Me….

The most revealing aspect of this debate is not the policy itself.

It is the sales campaign.

If these reforms were self-evidently beneficial, they would not require constant reassurance.

Australians are repeatedly being told the changes are good for them.

That they will solve affordability. That they will create fairness.

Perhaps they will – however I remain unconvinced.

But whenever governments need to spend more time marketing a policy than discussing its risks, unintended consequences and trade-offs, healthy skepticism is warranted.

After all, if a salesman, investment adviser, or real estate agent worked this hard to convince you, your first instinct would probably be to walk away...in fact to run away!

Maybe Australians should apply the same principle to public policy.

This particular policy should aim to create more homes, not destroy household wealth.

The real challenge is not making existing homes cheaper. The real challenge is building enough homes so prices stabilise naturally through increased supply rather than government intervention.

If it is such a great idea, why do they need to sell it so hard?